The FIRE Movement: How Tech Professionals in India Can Achieve Financial Independence by 45

By Immanuel Santosh | Certified Retirement Advisor

The gleaming towers of Bengaluru’s Electronic City and Mumbai’s Bandra-Kurla Complex house thousands of ambitious tech professionals earning salaries their parents could never have imagined. Yet despite these impressive paychecks, many are trapped in lifestyle inflation cycles that prevent them from achieving true financial independence. This comprehensive guide will show you exactly how to break free from the traditional work-until-60 mindset and achieve financial independence by 45 through the FIRE movement. We are

TL;DR – Key Takeaways

What is FIRE? Financial Independence, Retire Early (FIRE) is a movement focused on aggressive saving and strategic investing to achieve financial independence decades before traditional retirement age [1][2][3].

Why Tech Professionals? Tech professionals in India have unique advantages for FIRE including high earning potential, variable compensation, stock options, and rapid career growth, but also face challenges like income volatility and industry disruption [4][5].

Core Numbers: Most tech professionals need 25-40 times their annual expenses saved to retire early, depending on their chosen lifestyle. With disciplined saving rates of 50-70%, financial independence by 45 is achievable [1][6].

Key Strategies:

- Start aggressive saving immediately (aim for 50%+ savings rate)

- Maximize tax-advantaged accounts (PPF, EPF, NPS, ELSS)

- Build diversified investment portfolios heavy on equity

- Manage variable income systematically

- Avoid lifestyle inflation despite salary growth

Timeline: High-earning tech professionals can typically achieve FIRE in 10-15 years with proper planning and execution [7].

1. What is the FIRE Movement and Why Does it Matter for Tech Professionals?

2. How Much Money Do You Actually Need to Retire Early in India?

3. What Are the Different Types of FIRE?

4. How Do Tech Salaries in India Support FIRE Goals?

5. What Are the Common Pitfalls in Retirement Planning?

6. How Do I Create an Emergency Fund?

7. What About Healthcare Costs and Insurance?

8. How Do I Optimize Taxes for Early Retirement?

9. When Should I Start and What’s My Action Plan?

10. Frequently Asked Questions

What is the FIRE Movement and Why Does it Matter for Tech Professionals?

The FIRE movement represents a fundamental shift in how we think about work, money, and life priorities [2][4]. Unlike traditional retirement planning that assumes you’ll work until 60, FIRE focuses on achieving financial independence much earlier through aggressive saving and strategic investing.

For tech professionals in India, FIRE is particularly relevant because of the industry’s unique characteristics. The technology sector offers exceptional earning potential – a software engineer can progress from ₹5 lakhs annually to ₹50 lakhs+ within a decade [8][9][10]. However, this same industry also brings challenges like rapid skill obsolescence, variable compensation, and intense competition.

The beauty of FIRE for tech professionals lies in leveraging high incomes during peak earning years to build substantial wealth. Instead of gradually increasing lifestyle expenses with each promotion, FIRE practitioners maintain relatively modest lifestyles while investing the difference [5][11].

If you are looking for a detailed The Ultimate Retirement Planning Guide for GCC Professionals in India, you can click the link to read that report.

Why Traditional Retirement Planning Fails Tech Professionals

Traditional advice suggests saving 10-15% of income for retirement, but this approach assumes stable 40-year careers and predictable income growth [12][13]. Tech careers are different – they often involve:

- Rapid income growth followed by potential plateaus

- Variable compensation through bonuses and stock options

- Industry disruption that can shorten peak earning periods

- Higher stress levels that make early retirement more appealing

The FIRE movement addresses these realities by encouraging much higher savings rates (50-70%) during peak earning years, allowing for earlier exit from traditional employment [4][14].

How Much Money Do You Actually Need to Retire Early in India?

The cornerstone of FIRE planning is calculating your “FIRE number” – the amount you need invested to generate enough passive income to cover your expenses [1][6]. The most common approach uses the 4% rule, which suggests you can safely withdraw 4% of your investment corpus annually.

However, financial experts recommend Indian FIRE aspirants use a more conservative 3.5% withdrawal rate due to higher inflation and market volatility [1]. This means you need approximately 25-30 times your annual expenses saved to retire safely.

Real-World FIRE Numbers for Tech Professionals

Let’s examine realistic scenarios based on different lifestyle choices:

Conservative Lifestyle: ₹6-8 lakhs annual expenses

- FIRE number: ₹1.5-2.4 crores

- Suitable for: Single professionals or couples willing to live modestly

Comfortable Lifestyle: ₹12-15 lakhs annual expenses

- FIRE number: ₹3-4.5 crores

- Suitable for: Families wanting middle-class comforts without luxury

Affluent Lifestyle: ₹20-25 lakhs annual expenses

- FIRE number: ₹5-7.5 crores

- Suitable for: Those wanting to maintain high-income lifestyles

The key insight is that FIRE isn’t about extreme frugality – it’s about conscious spending aligned with your values while avoiding lifestyle inflation [6][11].

What Are the Different Types of FIRE?

The FIRE movement isn’t one-size-fits-all. Understanding different approaches helps you choose the path that aligns with your goals and risk tolerance [15][16][17].

Lean FIRE

Lean FIRE focuses on achieving financial independence with minimal annual expenses, typically ₹6-10 lakhs per year [15][16]. This approach requires:

- Extreme cost optimization

- Simple lifestyle choices

- Lower overall savings targets (₹1.5-3 crores)

- Higher risk of running out of money

Traditional FIRE

Traditional FIRE aims for comfortable middle-class retirement with annual expenses of ₹12-18 lakhs [15][16]. This balanced approach offers:

- Moderate lifestyle during accumulation

- Reasonable safety margins

- Corpus targets of ₹3-5.5 crores

- Good balance of sacrifice and security

Fat FIRE

Fat FIRE allows for luxury lifestyles with annual expenses of ₹25 lakhs or more [15][16]. This approach requires:

- Higher savings targets (₹6+ crores)

- Longer accumulation periods

- Higher incomes to support both lifestyle and savings

- Lower financial stress during retirement

Years to achieve different types of FIRE (Financial Independence, Retire Early) for tech professionals in India at various income levels and savings rates.

Barista FIRE

Barista FIRE represents partial financial independence where passive income covers basic needs, but part-time work provides lifestyle money [15][17]. This approach offers:

- Earlier escape from high-stress careers

- Flexibility to pursue passion projects

- Reduced savings requirements

- Income diversification in retirement

How Do Tech Salaries in India Support FIRE Goals?

Tech professionals in India enjoy exceptional earning potential that makes FIRE achievable within 10-15 years [8][9][10]. Understanding salary progression helps in realistic FIRE planning.

Entry-Level Professionals (0-3 years)

- Service companies: ₹3.5-8 lakhs annually

- Product companies: ₹8-20 lakhs annually

- Focus: Skill building and foundational investing

Mid-Level Professionals (4-8 years)

- Service companies: ₹8-16 lakhs annually

- Product companies: ₹25-75 lakhs annually

- Focus: Aggressive savings and portfolio building

Senior Professionals (8+ years)

- Service companies: ₹15-45 lakhs annually

- Product companies: ₹75 lakhs-2 crores annually

- Focus: Wealth optimization and FIRE preparation

The key advantage for tech professionals is rapid income growth. Someone starting at ₹5 lakhs annually can realistically reach ₹50+ lakhs within a decade through skill development and strategic career moves [9][10][18].

Variable Compensation Opportunities

Tech compensation often includes significant variable components that can accelerate FIRE timelines [19][18]:

- Annual bonuses: 10-50% of base salary

- Stock options: Potentially worth several years of salary

- Retention bonuses: Large one-time payments

- International assignment premiums

Smart management of these variable components can dramatically reduce time to FIRE [11].

How Do I Manage Variable Income and Stock Options?

Variable compensation is both an opportunity and a challenge for tech professionals pursuing FIRE [19][18][20]. The key is developing systematic approaches rather than treating bonuses as “extra” money.

Bonus Management Strategy

Create a predetermined allocation formula for bonus payments [11]:

- 60% to investments and FIRE goals

- 20% to other financial goals (home down payment, children’s education)

- 20% to lifestyle and discretionary spending

This ensures bonuses contribute meaningfully to wealth building while still allowing some lifestyle enhancement [11].

Stock Option Optimization

Stock options can create substantial wealth but require careful planning [18][20]:

Exercise Timing Considerations:

- Diversification needs (avoid over-concentration)

- Tax implications (ISO vs NQSO treatment)

- Market conditions and company prospects

- Personal liquidity requirements

Risk Management:

- Never let company stock exceed 20% of total portfolio

- Implement systematic selling schedules

- Consider hedging strategies for large positions

- Plan exercises around tax optimization

Income Smoothing Techniques

Variable income requires larger emergency funds and different budgeting approaches [20]:

- Maintain 9-12 months of expenses in emergency funds

- Budget based on base salary only

- Treat variable income as “investment acceleration”

- Use dollar-cost averaging for investment timing

What Investment Strategies Work Best for Tech Professionals? {#investment-strategies}

Tech professionals have unique advantages for building investment portfolios: high risk tolerance, long time horizons, and familiarity with growth companies [14][21][22]. However, they also face specific risks that require careful portfolio construction.

Core Portfolio Allocation

Age-based allocation provides a starting framework, but tech professionals can often be more aggressive due to high human capital [23]:

Ages 25-35: 80-85% equity, 15-20% debt

Ages 35-40: 70-75% equity, 25-30% debt

Ages 40-45: 60-70% equity, 30-40% debt

Recommended Investment Mix

Equity Investments (70-85% of portfolio):

- Large-cap mutual funds: 40-50% (stability and dividends)

- Mid-cap mutual funds: 20-30% (growth potential)

- Small-cap mutual funds: 10-15% (high growth, high risk)

- Index funds: 20-25% (low-cost market exposure)

- International funds: 10-15% (geographic diversification)

Debt Investments (15-30% of portfolio):

- PPF: Maximum allowed (₹1.5 lakhs annually)

- EPF: Mandatory contribution plus voluntary PF

- Debt mutual funds: Short to medium-term funds

- Fixed deposits: Only for emergency funds

Alternative Investments (5-10% of portfolio):

- REITs: Real estate exposure without direct ownership

- Gold ETF: Inflation hedge and portfolio diversification

- International exposure: Developed and emerging markets

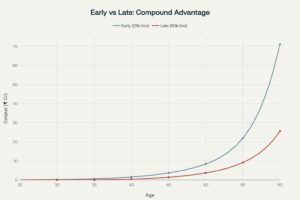

Comparison of investment corpus growth between starting SIP investments early (₹25,000/month at age 25) vs. starting late with higher amount (₹50,000/month at age 35)

Systematic Investment Plan (SIP) Strategy

SIPs are particularly powerful for tech professionals due to income volatility [21][22][24]. Current SIP trends show monthly contributions of ₹26,000+ crores, indicating strong investor confidence [22][24].

SIP Best Practices:

- Start with conservative amounts and increase annually

- Use step-up SIPs to match salary growth

- Diversify across different fund categories

- Never stop SIPs during market downturns

- Review and rebalance quarterly

Tax-Efficient Investing

High-earning tech professionals must prioritize tax efficiency [25][23]:

Section 80C Investments (₹1.5 lakhs limit):

- ELSS mutual funds: Tax saving + equity growth

- PPF: 15-year lock-in, tax-free returns

- Life insurance: Term plans only, avoid ULIPs

Additional Tax Benefits:

- NPS: Additional ₹50,000 deduction under 80CCD(1B)

- Health insurance: Deductions under Section 80D

- Home loan: Interest deduction under 24(b)

What Are the Common Pitfalls in Retirement Planning?

Even smart tech professionals make predictable mistakes that can derail FIRE goals [26][27][28][29]. Understanding these pitfalls helps avoid costly errors.

Lifestyle Inflation

The biggest threat to FIRE goals is increasing expenses faster than income [28][30]. Common lifestyle inflation triggers:

- Moving to expensive neighborhoods after promotions

- Upgrading cars, gadgets, and vacations automatically

- Social pressure in tech hubs like Bangalore and Gurgaon

- Believing higher income justifies higher spending

Solution: Maintain fixed expense ratios regardless of income growth. If you can live well on ₹60,000 monthly at ₹15 lakhs annual income, you can live excellently on ₹100,000 monthly at ₹25 lakhs income while saving the difference [28].

Over-Concentration in Company Stock

Tech professionals often accumulate large positions in employer stock through options and ESPP programs [20][31]. This creates dangerous concentration risk where both employment income and investment returns depend on one company.

Solution: Implement systematic diversification rules – never let any single stock exceed 10-15% of total portfolio [20].

Underestimating Healthcare Costs

Healthcare inflation in India runs at 13-14% annually, well above general inflation [32][33]. Many FIRE aspirants underestimate future medical expenses, particularly after age 50.

Solution: Budget ₹3-5 lakhs annually for healthcare in retirement, with 6-8% annual increases [12][34][32]. Invest in comprehensive health insurance with family floater coverage of ₹15-25 lakhs.

Starting Too Late

Compound interest rewards early starters disproportionately. Delaying FIRE planning by even 5 years can add 10+ years to the timeline [30][26].

Starting Too Conservative

Young tech professionals often invest too conservatively, missing out on equity growth during their highest risk tolerance years [29][35]. Fixed deposits and traditional insurance policies can’t generate returns needed for FIRE.

Solution: Embrace appropriate risk during accumulation phase. Equity mutual funds, despite volatility, have consistently outperformed inflation over long periods [36].

How Do I Create an Emergency Fund?

Emergency funds are crucial for tech professionals due to industry volatility and variable income [34][37]. Unlike stable government jobs, tech careers can face sudden layoffs, economic downturns, or company-specific challenges.

Emergency Fund Size

Tech professionals need larger emergency funds than traditional recommendations [37]:

- Minimum: 6 months of expenses

- Recommended: 9-12 months of expenses

- High-risk roles: 12+ months of expenses

Emergency Fund Calculation Examples

For professionals with ₹75,000 monthly expenses:

- 6-month fund: ₹4.5 lakhs

- 9-month fund: ₹6.75 lakhs

- 12-month fund: ₹9 lakhs

Where to Keep Emergency Funds

Emergency funds must balance safety, liquidity, and returns [38]:

- High-yield savings accounts: 6-7% returns, instant access

- Liquid mutual funds: 6-8% returns, 1-day redemption

- Short-term FDs: 7-8% returns, penalty for early withdrawal

- Sweep-in FDs: Automatic conversion, good liquidity

Building Your Emergency Fund

Step 1: Calculate target amount based on monthly expenses

Step 2: Open dedicated high-yield savings account

Step 3: Set up automatic monthly transfers

Step 4: Avoid using for non-emergencies

Step 5: Replenish immediately after any withdrawals

What About Healthcare Costs and Insurance?

Healthcare represents one of the largest uncontrolled expenses in retirement [12][34][32][33]. With medical inflation at 13% annually and increasing life expectancy, proper healthcare planning is essential for FIRE success.

Health Insurance Strategy

Employer Insurance: Maximize employer coverage while employed, but don’t rely on it post-retirement [34][39].

Personal Health Insurance: Purchase comprehensive coverage early for lower premiums and pre-existing condition coverage [34][27]:

- Individual coverage: ₹10-15 lakhs

- Family floater: ₹15-25 lakhs

- Super top-up: Additional ₹25-50 lakhs

Critical Illness Insurance: Separate coverage for heart disease, cancer, stroke – conditions common after 40 [34][37].

Healthcare Cost Planning

Budget significant amounts for healthcare in FIRE calculations [32][33]:

- Ages 45-55: ₹2-3 lakhs annually

- Ages 55-65: ₹4-6 lakhs annually

- Ages 65+: ₹6-10 lakhs annually

These amounts should increase by 6-8% annually to account for medical inflation [32][33].

Health Savings Strategy

Create separate healthcare corpus alongside main FIRE corpus:

- Target: ₹50-75 lakhs dedicated healthcare fund

- Investment: Conservative debt funds for capital protection

- Usage: Medical expenses not covered by insurance

How Do I Optimize Taxes for Early Retirement?

Tax optimization becomes increasingly important as incomes grow [25][23][20]. High-earning tech professionals can save substantial amounts through strategic planning.

Maximizing Deductions

Section 80C (₹1.5 lakhs limit):

- PPF: Best long-term option for tax-free growth

- ELSS: Shortest lock-in with equity growth potential

- Life insurance: Only term plans, avoid traditional policies

- EPF/VPF: Additional voluntary contributions

Section 80CCD(1B) (₹50,000 limit):

- NPS contributions: Additional tax benefit beyond 80C

- Equity exposure: Choose aggressive allocation for growth

Other Deductions:

- Health insurance: Section 80D

- Home loan interest: Section 24(b)

- Education loan interest: Section 80E

Capital Gains Optimization

Long-term Capital Gains (LTCG):

- Hold equity investments for 1+ years

- ₹1 lakh annual exemption for equity LTCG

- 10% tax rate above exemption limit

Tax-Loss Harvesting:

- Realize losses to offset gains

- Maintain portfolio allocation through fresh purchases

- Particularly valuable in volatile years

Withdrawal Strategy in Retirement

Plan post-FIRE withdrawals for tax efficiency:

- Years 1-5: Tax-free sources (PPF partial withdrawals, EPF)

- Years 6-10: Low-tax sources (equity LTCG up to exemption)

- Years 10+: Balanced approach across all sources

When Should I Start and What’s My Action Plan?

The best time to start FIRE planning is now, regardless of your current age or income level [26][30]. However, your specific strategy should align with your career stage and financial situation.

Immediate Actions (Next 30 Days)

Week 1-2:

- Calculate current net worth and monthly expenses

- Determine FIRE number based on desired lifestyle

- Open high-yield savings account for emergency fund

- Review and optimize current employer benefits

Week 3-4:

- Open demat account with reputable broker

- Start basic SIPs in large-cap equity funds

- Maximize employer EPF matching

- Purchase adequate term life insurance

First Year Priorities

Months 1-3:

- Build emergency fund to 6 months of expenses

- Establish automatic investment systems

- Maximize tax-advantaged account contributions

- Track expenses rigorously to identify optimization opportunities

Months 4-6:

- Expand investment portfolio with mid-cap and international funds

- Increase SIP amounts with any salary hikes or bonuses

- Review and upgrade insurance coverage

- Begin learning about advanced investment strategies

Months 7-12:

- Build emergency fund to 9-12 months of expenses

- Implement tax-loss harvesting strategies

- Consider real estate or REIT investments

- Plan next year’s financial goals and adjustments

Long-term Milestones

Year 2-3: Achieve consistent 50%+ savings rate

Year 5: Reach first ₹1 crore in investments

Year 7-10: Cross halfway point to FIRE number

Year 10-15: Achieve full FIRE and transition planning

Monitoring Progress

Monthly Reviews:

- Track expenses vs. budget

- Monitor investment performance

- Assess progress toward annual goals

- Adjust strategies based on results

Annual Reviews:

- Comprehensive portfolio rebalancing

- Update FIRE calculations for inflation

- Review and update insurance coverage

- Tax planning and optimization

- Career progression assessment

FIRE Action Checklist for Tech Professionals in India

Phase 1: Foundation Building (Immediate Actions)

Emergency Fund Setup

-

Calculate 6-9 months of expenses

-

Open high-yield savings account

-

Set up automatic transfer for emergency fund

-

Target: ₹3-6 lakhs for most tech professionals

Basic Insurance Coverage

-

Get comprehensive health insurance (₹10-20 lakhs coverage)

-

Purchase term life insurance (10x annual income)

-

Consider personal accident insurance

-

Review and update all insurance annually

Income Optimization

-

Negotiate salary during appraisals

-

Optimize variable compensation strategy

-

Plan stock option exercises strategically

-

Develop skills for career advancement

Phase 2: Investment Setup (Month 1-3)

Tax-Advantaged Accounts

-

Maximize EPF contribution

-

Open and contribute to PPF (₹1.5 lakhs annually)

-

Consider NPS for additional tax benefits

-

Invest in ELSS for 80C benefits

Core Investment Portfolio

-

Open demat and trading account

-

Start SIP in large-cap mutual funds

-

Add mid-cap funds gradually

-

Include index funds for low-cost exposure

-

Set up international fund SIPs

Automation Setup

-

Automate all SIP investments

-

Set up automatic bill payments

-

Create systematic savings transfers

-

Use apps for expense tracking

Phase 3: Wealth Acceleration (Ongoing)

Portfolio Diversification

-

Maintain age-appropriate asset allocation

-

Rebalance portfolio quarterly

-

Review and adjust risk tolerance

-

Consider alternative investments (REITs, gold)

Income Diversification

-

Develop consulting/freelance skills

-

Create passive income streams

-

Explore side businesses

-

Build professional network

Tax Optimization

-

Implement tax-loss harvesting

-

Plan capital gains realization

-

Optimize bonus and stock income timing

-

Consider tax-efficient withdrawal strategies

Phase 4: FIRE Preparation (5 years before target)

Corpus Calculation

-

Calculate exact FIRE number

-

Plan for healthcare cost inflation

-

Consider lifestyle inflation factors

-

Build buffer for market volatility

Income Transition

-

Reduce lifestyle inflation

-

Test lower expense scenarios

-

Develop post-FIRE income plans

-

Explore passion projects/businesses

Risk Management

-

Increase health insurance coverage

-

Consider long-term care insurance

-

Update estate planning documents

-

Review beneficiary nominations

Monthly Review Checklist

-

Track expenses and savings rate

-

Monitor investment performance

-

Review emergency fund adequacy

-

Check progress toward FIRE goals

-

Adjust strategies as needed

Annual Review Checklist

-

Comprehensive portfolio review

-

Update FIRE calculations

-

Review and update insurance coverage

-

Tax planning and optimization

-

Career progression assessment

-

Investment allocation rebalancing

Key Warning Signs to Watch

-

Savings rate dropping below 30%

-

Lifestyle inflation exceeding income growth

-

Over-concentration in company stock

-

Inadequate emergency fund

-

Poor investment performance vs. benchmarks

Success Metrics to Track

-

Net worth growth rate

-

Savings rate percentage

-

Investment returns vs. inflation

-

Time to FIRE target

-

Monthly passive income generated

Remember: FIRE is a marathon, not a sprint. Consistency and discipline matter more than perfect timing or maximum returns.

Frequently Asked Questions

Q: Can I achieve FIRE with a ₹15 lakh salary?

A: Yes, but it requires aggressive saving and longer timelines. Focus on maximizing savings rate (aim for 60%+), living modestly, and choosing Lean FIRE targets. Consider increasing income through skill development and job changes [8][9][10].

Q: Should I buy a house or rent while pursuing FIRE?

A: In expensive cities like Mumbai and Bangalore, renting often makes more financial sense during FIRE accumulation. Use saved capital for investments rather than real estate down payments. Consider buying only if the property cash flows positively [28].

Q: What if there’s a major market crash near my FIRE date?

A: Build flexibility into your FIRE plan. Maintain 2-3 years of expenses in conservative investments. Consider “Coast FIRE” where you have enough saved that natural growth will fund later retirement even if you stop saving [17].

Q: How do I handle family pressure about “risky” investing?

A: Education is key. Share historical data on equity returns and inflation impact. Start conservatively and increase equity exposure gradually. Consider involving family in investment education [13][40].

Q: What about children’s education costs?

A: Plan separately for education expenses. Don’t raid FIRE corpus for education needs. Consider education loans which offer tax benefits under Section 80E [28].

Q: Should I quit my job immediately after reaching my FIRE number?

A: Consider a gradual transition. Try sabbaticals, part-time work, or passion projects before fully retiring. This helps test your financial plan and adjust to non-working life [16][17].

Q: What if I change my mind about early retirement?

A: FIRE planning provides options, not obligations. Having financial independence means you can choose to work or not work based on passion rather than necessity [4][5].

Q: How do I account for inflation in my FIRE planning?

A: Use conservative withdrawal rates (3.5% instead of 4%) and build buffers into your calculations. Invest in inflation-beating assets like equity mutual funds and REITs [1][14].

Q: What’s the biggest mistake people make pursuing FIRE?

A: Underestimating healthcare costs and being too aggressive with withdrawal rates. Always build safety margins into your calculations [12][34][32][33].

Q: Can I still enjoy life while saving 50-70% of income?

A: Absolutely. FIRE is about conscious spending on things that truly matter while eliminating waste. Many find greater happiness through intentional living than mindless consumption [4][5][11].

The journey to financial independence by 45 is challenging but absolutely achievable for dedicated tech professionals in India. Start today, stay consistent, and remember that every month of delay adds years to your timeline. Your future self will thank you for the discipline and sacrifice required to achieve true financial freedom. If you want more help implementing this, here is a detailed information.

Author – Immanuel Santosh

Immanuel Santosh is a Chartered Insurance & Succession Planner from American Association for Financial Management (India Chapter) with 15+ years of experience specializing in retirement planning for technology professionals. He is also a Certified Retirement Advisor as prescribed by NISM, India and has recently cleared his QPFP examination from NetworkFP India.

⁂

- https://www.indiatoday.in/business/personal-finance/story/early-retirement-age-40-savings-needed-corpus-inflation-fire-trend-financial-independence-2743639-2025-06-20

- https://www.iibf.org.in/documents/BankQuest/October-December 2024/12.pdf

- https://www.hdfclife.com/insurance-knowledge-centre/retirement-planning/what-is-fire-and-how-does-it-work

- https://www.linkedin.com/pulse/fire-movement-india-can-you-retire-early-deepak-pincha-kxz0f

- https://mylifexp.com/parenting/retire-young-retire-rich-the-rise-of-fire-in-india/articleshow/119792466.html

- https://wire.insiderfinance.io/how-to-retire-early-in-india-a-step-by-step-plan-to-achieve-financial-independence-dc53d05b757b?gi=e4bb53292bea

- https://www.besanttechnologies.com/it-salary-in-india

- https://fello.in/blogs/how-to-retire-early-in-india

- https://www.torusdigital.com/toruscope/investing/financial-independence-fire-movement-india/

- https://economictimes.indiatimes.com/fire-myth-financial-independence-retire-early-sounds-glamorous-it-takes-much-more-than-mere-ambition/editionlist/edition-121850472,artid-121845524.cms?from=mdr

- https://www.payscale.com/research/IN/Job=Software_Engineer/Salary

- https://www.levels.fyi/t/software-engineer/locations/india

- https://www.upgrad.com/blog/software-engineer-developer-salary-in-india-freshers-experienced/

- https://www.reddit.com/r/developersIndia/comments/10jwmg3/how_much_are_software_engineers_making_in_india/

- https://www.levels.fyi/companies/glance/salaries/software-engineer/locations/india

- https://economictimes.indiatimes.com/tech/information-tech/variable-pay-attrition-moonlighting-it-firms-grapple-with-a-mix-of-problems/articleshow/93779656.cms

- https://www.levels.fyi/companies/amazon/salaries/software-engineer/locations/india

- https://www.youtube.com/watch?v=awagIYHzoA4

- https://in.talent.com/salary?job=software+engineer

- https://economictimes.com/tech/information-tech/variable-pay-attrition-moonlighting-it-firms-grapple-with-a-mix-of-problems/articleshow/93779656.cms

- https://www.righthorizons.com/blogs/challenges-in-retirement-planning-navigating-the-financial-future-in-india/

- https://lifeinsurance.adityabirlacapital.com/articles/retirement-insurance/overcoming-your-5-biggest-retirement-challenges/

- https://moneyandme.pgimindiamf.com/save-invest/articles/10-Retirement-Challenges-and-Their-Solutions

- https://www.morningstar.in/posts/76603/much-works-required-to-improve-retirement-in-india.aspx

- https://economictimes.indiatimes.com/jobs/indian-employees-inadequately-prepared-for-retirement-survey/articleshow/51042091.cms

- https://www.coveryou.in/blog/rising-medical-inflation-rate-in-india/

- https://www.5paisa.com/stock-market-guide/tax/how-to-save-income-tax-in-india

- https://timespro.com/blog/maximising-your-savings-how-to-choose-between-ppf-and-epf

- https://www.mdrt.org/learn/2025/html/retirement-planning-trends-for-an-aging-india

- https://www.financialexpress.com/business/healthcare/indias-healthcare-costs-to-rise-13-in-2025-beat-global-average-report/3800929/

- https://www.reddit.com/r/Fire/comments/1heki4b/whats_the_standard_of_lean_fire_traditional_fire/

- https://www.indiafirstlife.com/knowledge-center/retirement-planning/what-is-the-fire-method

- https://hospitality.economictimes.indiatimes.com/news/speaking-heads/from-aspiration-to-reality-millennials-and-the-fire/112212744

- https://www.youtube.com/watch?v=YQZxAlWplno

- https://earnkaro.com/blog/side-hustles-in-india/

- https://www.business-standard.com/markets/mutual-fund/mutual-fund-sip-strategy-continue-to-invest-or-hit-the-pause-button-125021300684_1.html